Company Registration Online in India | Filing Done in 7-10 Days

Register your company online in India, Private Limited, LLP, OPC, Public Limited, Section 8, and more. Our CA-assisted process includes DSC, DIN, name approval, MOA/AOA drafting, and MCA filing from start to finish. Applications are filed within 7 to 10 working days. Get fast and hassle-free company registration in india with us, so you can focus on growth while we take care of the paperwork.

- Working Days

- 2 Directors Minimum

- Foreign Investment

- Government Schemes Access

- 100% Online - MCA Portal

Everything included in your Online Company registration package

- Pvt Ltd, LLP, OPC, Section 8

- DSC and DIN Number

- Company Name Reservation

- Drafting of MOA and AOA

- PAN Card & TAN Application

- Compliant and Investor-ready Business

- Certificate of Incorporation

Request a Callback

4.9 star all time rating

4.8 star all time rating

COMPANIES ACT

What is Companies Act 2013? (And Why it Matters for Registration)

The Companies Act 2013 is the primary law governing the formation, operation, and dissolution of companies in India. Enacted by Parliament on August 29, 2013, it replaced the Companies Act 1956 to simplify, digitize, and align corporate governance with international standards.

The Companies Act 2013 plays a significant role in company registration, making the process uniform and easy across the country.

The Act requires all companies, whether private, public, or individual, to register under its rules to ensure proper legal identity and accountability. It includes key features such as digital filing, SPICE+ (Easy Proforma Plus for Electronic Incorporation of a Company) forms, quick online registration, and a one-stop portal for faster and more efficient access to all necessary approvals.

Compliance under the Companies Act 2013 is not just a legal formality but a protection from penalties and operational hurdles, allowing them to operate with confidence in the Indian business environment.

OVERVIEW

What is Company Registration?

Company Registration in India is the legal process of incorporating a business entity under the Companies Act 2013 and obtaining a Certificate of Incorporation from the MCA (Ministry of Corporate Affairs). This gives the company a separate legal identity, limited liability protection, and the ability to enter into contracts, open bank accounts, and raise investments.

Being a registered company builds credibility with customers, partners, and investors. It also makes your business eligible for funding and protects your brand value.

JustStart handles the entire company registration process from start to finish, from choosing the right structure and reserving your company name, to filing with the MCA and receiving your Certificate of Incorporation, PAN, and TAN. Over 5,000 companies are registered.

Business Structures

Business Structure Comparison Table

When starting a company, choosing the right business structure is one of the crucial first steps, according to your size and investment in your business. Use the comparison table below to understand in which business structure your business/entity falls:-

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

STRUCTURES

Types of Company Registration in India

Choosing the right company structure is crucial to your growth plans and business success. Here's a simple overview of the main types of company structures in India:

Each business structure has its own unique advantages; choose the structure that best suits your vision, size, and compliance needs.

Private Limited Company (Pvt Ltd)

A private limited company is the best structure for startups and small to medium-sized enterprises. It provides limited liability, a separate legal identity, and attracts investors. It is reliable and widely used in India.

Limited Liability Partnership (LLP)

An LLP (Limited Liability Partnership) is ideal for professionals and small business partners who want to start a business with their partner, as it combines the benefits of a partnership and a company. It offers flexibility in management, and partners enjoy limited liability with fewer compliances.

One Person Company(OPC)

A One Person Company is ideal for individuals who want to run a company with limited liability and complete control. It offers the benefits of a private limited company without the need for a partner.

Section 8 Company (NGO)

Section 8 Companies are designed for non-profit organizations and social enterprises. These companies don't focus on profit and receive several tax benefits for their work for the community.

Public Limited Company (LTD)

A Public Limited Company is ideal for larger businesses that want to raise money from the public or list on the stock market. It attracts public investment.

Producer Company(FPO)

Farmer-Producer Companies are great for farmers or those involved in agriculture. They help members work together in farming, production, processing, and marketing, providing better market access and profit sharing.

Documents Required

Documents Required for Company Registration Online

In India, registering a company means submitting the correct documents is mandatory. Mistakes or missing paperwork will lead to rejection and delays. Here’s a list of documents required for company registration online:

Documents Needed for Indian Directors/ Shareholders

- PAN Card: Mandatory for identity verification

- Aadhaar: Required for KYC and digital verification

- Address Proof: Address proof like voter ID card, driving license or passport, bank statement

- Photographs: Recent passport-size photo with clear background.

- Utility Bill( Business Address proof): Latest electricity bill, water or gas bill of the premises ( not older than 2 months)

- NOC from Property Owner: If the premises are on rent, then the rent agreement or the NOC from the owner is required.

- MOA: Memorandum of Association describes the business objects.

- AOA: Article of Association describes how the company will operate internally.

Documents Required for Foreign Nationals:

- Passport - Valid, notarised & apostilled

- Address Proof: Notarised & apostilled

Common Mistakes to Avoid:

- Cross-verify the documents while submitting the forms, like spelling mismatches in the PAN card or the Aadhar card.

- Using an old utility bill.

- Uploading unsigned documents

- Submitting foreign documents ( Notarised & Apostilled)

Getting your right documents from the start saves your time and prevents unnecessary hassle. At JustStart, we help you review and organise all paperwork for smooth functioning and error-free company registration.

Benefits

Benefits of Registering a Company in India

Registering a company has many benefits in terms of limited liability, investment, funding, etc. Here are the benefits of online company registration in India:-

Legal Recognition:

A registered company has a legal recognition. It can sign contracts, get funding, and apply for government tenders.

For Example, A software developer started as a freelancer. After registering the company, he can sign contracts with big IT companies.

Limited liability Protection:

If the company faces any legal problem, the director’s/partner’s personal money and property are safe.

For Example: If your business loses money, your personal assets like a car, houses won’t be taken to pay the company’s debt.

Foreign Investment:

Foreign investments are made easier when the person has a registered company, as the investment from the foreign investors under the automatic route can be taken, especially for private limited companies.

For Example: A Bangalore based app development company got seed funding from a US investor after registering as a Private Ltd Company.

Brand Protection:

Once your company is registered, no one else can legally use the name or a similar name to register a company with a similar name. It can protect your brand name and legal identity.

For Example: Oh My Vegan protects their brand by copying from other brands by registering it with MCA.

Perpetual Succession:

A company which is registered keeps running if the owner leaves, retires or passes away. It means it never ends. It has a perpetual succession.

For Example: ABC is a private limited company. There are 2 directors in an ABC Private company. Director 2 left the company due to some personal issues. So, the company continues by appointing another director in an ABC Private Limited Company.

Tax Benefits:

Pay less, Save more: A registered company in India has many special tax deductions, rebates and lower tax rates in terms of unregistered companies.

For Example: a Private Limited Company, A startup registered in Mumbai, earned ₹35 lakhs profit. Because it was a DPIIT-recognized startup under Startup India, it claimed the 3-year tax holiday and paid zero income tax in the first 3 years.

Access to Government Schemes:

Registered companies can apply for MSME status, Startup India recognition (DPIIT), and government tenders, which are not available to unregistered businesses.

Eligibility

Eligibility Criteria for Company Registration in India

Before registering a company, it is very important to know the Eligibility criteria for company Registration and what are the requirements must be met:

✅ Minimum Age:

Directors must be at least 18 years in age, and there is no maximum age limit for registering a company in India.

✅ Nationality:

Indian citizens, Non-resident Indians, and Foreign Nationals can register a company in India. In case of foreign nationals must provide a valid passport and address proof.

✅ Minimum directors/members for each structure:

- Depending on the business structure, the minimum number of directors varies. They are :

- Private Limited company: Minimum 2 directors, 2 shareholders

- Public limited company: Minimum 3 directors, 7 shareholders

- One-person Company: Minimum 1 director, 1 shareholder

- Limited Liability Partnership (LLP): Minimum 2 Designated partners

✅ Restrictions for undischarged insolvents or persons convicted of fraud:

- Persons who are involved in any illegal activity.

- People who haven’t cleared bankruptcy

- Has any person conducted any fraud or misconduct in the last 5 years

- Disqualified by a court or any government regulatory body.

Process

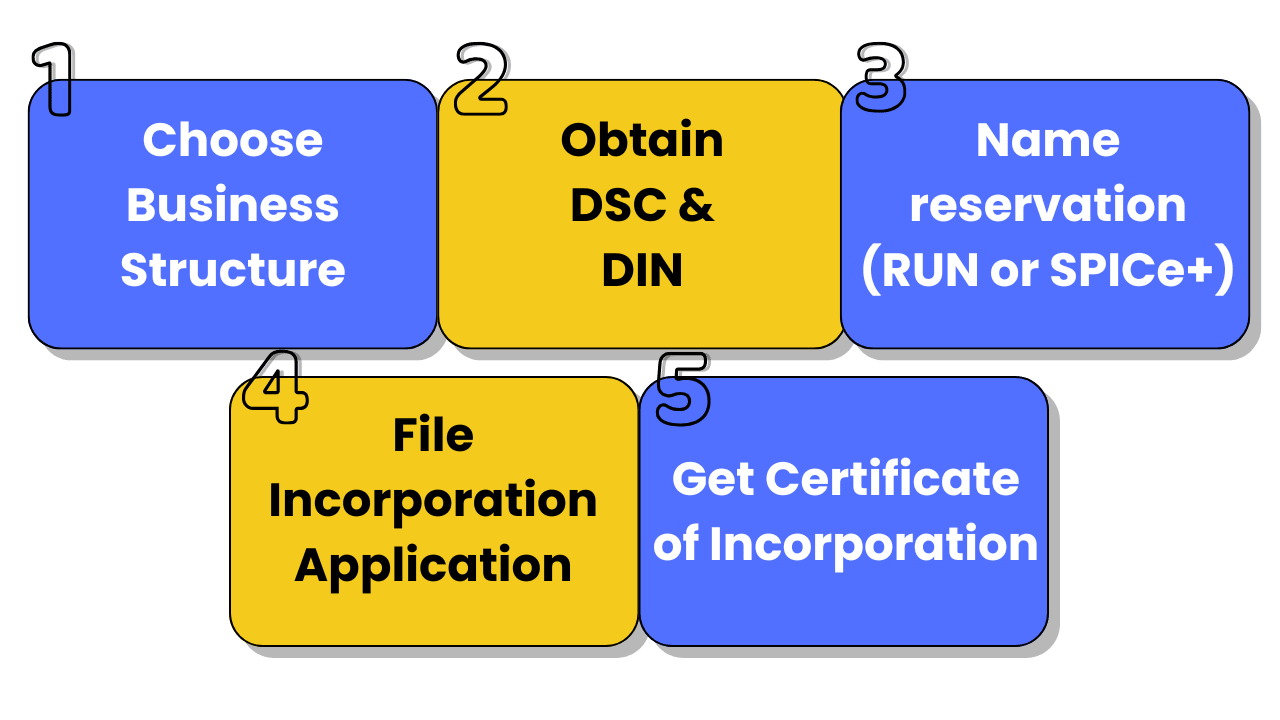

How to Register a Company Online in India - Step-by-step Process

Starting a company registration in India involves following the legal steps. Here, it is:

Step 1: Choose the Right Business Structure

First, choose the right business structure, such as a Pvt Ltd Company, OPC, LLP, or Public Limited Company (PLC). Your choice of business structure will impact your tax liability, compliance, fundraising ability, and ownership flexibility.

Step 2: Obtain DSC & DIN

Then, obtain the Digital Signature Certificate (DSC) and director identification number (DIN) of the proposed directors/partners. This is one of the essential steps in company registration.

Step 3: Name reservation (RUN or SPICe+)

Now choose a unique name for your company and fill out a form for name reservation. It should not be similar to the existing companies and registered trademarks.

Step 4: Prepare MOA & AOA

Prepare a MOA( Memorandum of Association ) explaining the business activities of the company, and an AOA( Articles of Association) that defines the company's rules and structure.

Step 5: File incorporation application

The next step is to prepare the Spice+ forms after preparing all the above documents with all the attachments required for filling the forms.

Step 6: Get Certificate of Incorporation, PAN, TAN

After submitting the form, if all the forms are approved by the ROC, then we will get the Certificate of Incorporation, PAN and TAN of the company.

Step 7: Apply for GST( Goods & Services Tax)

It is optional to get the GST registration number. If your turnover exceeds Rs. 20 lakhs for service providers and for goods it exceeds Rs. 40 lakhs, then it will be mandatory to get the registration certificate.

With JustStart, you don't have to worry about paperwork or processes; every step is handled by a team of experts, so you can focus solely on growing your business.

Name Reservation

Business Name Reservation

Choosing your business name is the first and most important step in the company registration process. It should be a unique name not resembling any existing companies and registered trademarks, general names, or contain any restricted words. This helps you to build your brand identity and avoid legal issues.

There are 2 ways to reserve the name on the MCA

RUN (Reserve unique name) - Run is the form when you choose to reserve your name first and then start the process. Or SPICE+ - you are ready to register the company along with the name.

Here are some simple Tips for name approval under MCA rules

- Ensure Uniqueness: Keep it simple and unique to be free from any hassle with the name.

- Avoid Restricted Names: Don’t take general names or any restricted names like Bank, insurance, stock exchange, mutual funds, etc, which require special approvals.

- Use a Proper Suffix: Add a proper suffix after your company based on the business type, like private limited company, limited liability partnership (LLP), OPC for One person Company & public limited company for public companies.

- Avoid Names that Sound too Generic: Names like SPECIAL TRADERS LLP or General Traders should be avoided.

_1762157834.webp)

Before you apply for name reservation, make your name by following the tips for name approval. At JustStart, we can help you to register your name with proper confidentiality.

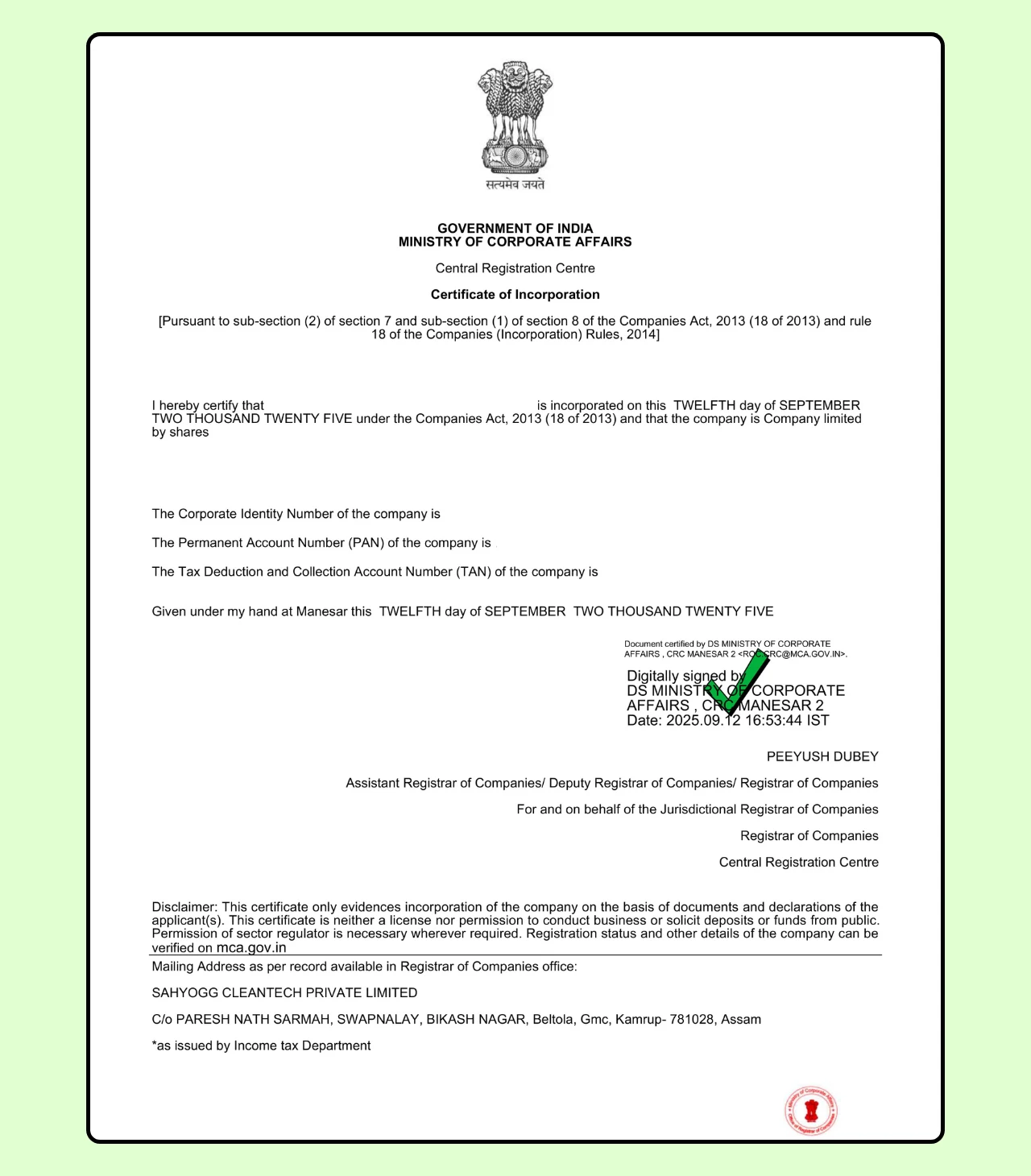

Certificate

What is a Company Registration Certificate?

An official document issued by the ROC (Registrar of Companies) signifies that your enterprise is legally registered as per Indian law, called the “Certificate of Incorporation”. It is also known as Registration Certificate, and it marks the finalisation of all incorporation formalities.

The Certificate of Incorporation contains all the legally required information about a company, such as the company's official name, registered address, date of incorporation, etc., as well as a unique corporate identification number called the "CIN Number." The CIN is a 21-digit alphanumeric number assigned to every company at the time of incorporation, which provides a host of information about the company, such as the type of company, the year it was incorporated, the state in which it was registered, the company's industry classification, and the registration sequence number.

The Certificate of Incorporation is the most important document for a company; it is the legal proof of its existence, allowing it to open a bank account, enter into contracts, and conduct business.

Compliances

Essential Post-Registration Compliance

After incorporating your company in India, it's necessary to file post-registration compliances. This depends on the specific business structure chosen. However, the following are the essential post-registration compliances:

1. Commencement of Business Form: Form Inc-20 will be filed for the commencement of business within 6 months from the date of Incorporation.

2. Director’s KYC: DIR-3KYC form should be filed every year for updating the information of the directors/partners.

3. Return of Deposits: Form DPT-3 requires information on deposits and non-deposits taken by the Company. If there are no deposits, then it is not mandatory to file the form.

4. Appointment of Auditor: Form ADT-1 filed for the appointment of an auditor in the company who will sign the financials of the company.

5. Financial Statement Return & Annual Return: Form AOC-4 & MGT-7 are the most important forms for the company disclosures regarding the audited financial statements & annual return of the company.

6. Income Tax Return: Every company has to file an income tax return every year

7. Other Compliance: Based on the business activities, it depends on the objects taken. Suppose a company engaged in the food business requires FSSAI licence, an importer-exporter requires an IEC number, and the GST holder complies with the GST compliances.

Why Choose JustStart?

Why 5000+ Founders Choose JustStart for Company Registration?

Starting a business is fun, but it's not as easy as entrepreneurs think. At JustStart, we make company registration fast, easy, and stress-free so entrepreneurs can focus on growth instead of compliance.

Fast Processing Time

Our experts complete the process very fast, helping you register your company without any unnecessary delays.

No Hidden Charges

Our prices are transparent, and there are no hidden charges. With JustStart, you get clear and upfront pricing so that you always know what you are paying for.

Expert Team of Professionals

JustStart is having a team of qualified professionals who understand your business requirements and then will start the process.

End-to-end Support

We not only incorporate your business, we assist even with the post-registration compliances so that your business will run smoothly without any delays and avoid huge penalties.

Structured Compliance Services

At JustStart, we can curate your compliance packages according to your business requirements.

Proven Track Record

5000+ companies registered across India since 2021. 4.8/5 on Google Rating and 4.8/5 on Trustpilot.

JustStart is your trusted partner for complete compliance

support and online company registration - all in one place!

Locations

Company Registration in Other States and Cities

FAQs

LET'S CLEAR ALL THE DOUBTS!

There is no minimum paid-up capital required to register a company in India. You can register your company by just putting a small capital amount of ₹1000, also, allowing it to be accessible to startups and small businesses.

Registration of a company generally takes 7–10 days, depending on how complete your documents are and the Ministry of Corporate Affairs (MCA) approval process.

Foreign nationals can indeed register a company in India. At least one director should be an Indian resident, and the applicant must furnish a handful of mandatory documents, such as valid identification and proof of address, besides incorporation-related documents.

Click here to read more about Company Registration for Foreigners & NRIs

Some of those compliances would include:

- Filing annual returns with MCA

- Maintaining books of accounts and financial statements along with auditor's report

- Charging GST on applicable services/products

- Obtaining licenses as per the industry being ventured by the company

Yes, you can convert an existing sole proprietorship to a private limited company. This involves incorporation of a new company, the transfer of assets and liabilities, and completing formalities with the MCA.

Click here to find out which is better for your business- Sole Proprietorship vs Private Limited Company

The office address must be registered in the company registration online. However, it may also be a virtual office meeting all the legal requirements and MCA regulations.

Click here to read more about Company incorporation without Physical Office.

Non-compliance with the post company registration requirements can be penalized with late fees; the corporation can also risk getting struck off the register. An essential thing to maintain for keeping your company legally alive is to stay updated regarding annual filings and statutory requirements.

Using JustStart for company registration will give you fast and hassle-free registration services with expert guidance every step of the way. Moreover, it will offer transparent pricing, with no hidden costs, leading to a stress-free experience from start to finish.

A Certificate of Incorporation is an official document issued by the Ministry of Corporate Affairs when a company is registered. It proves that the company is legally recognized and includes details like the company name, registration number, and date of incorporation.

In India, a Private Limited Company enjoys the status of an irreversible one. It can, thus, continue to exist even after a change of directors and shareholders, which provides a certainty of long-term continuity for a particular business.

After receiving the Certificate of Incorporation, PAN and other registration documents, you can go to any bank to open a current account in the name of your company. These documents act as proof of the legal existence of the concerned company.