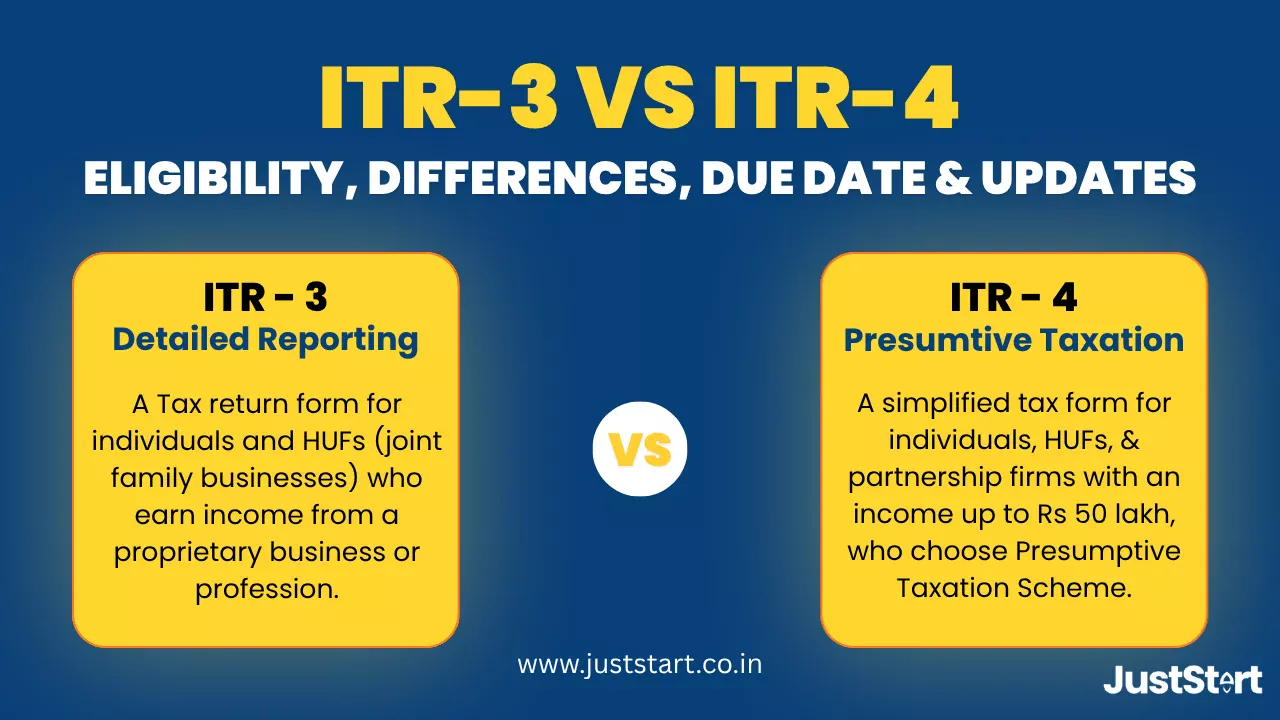

Individuals or Hindu Undivided Families whose source of income is from a proprietary business or profession file the ITR-3. The applicable taxpayers who file ITR-3 are required to maintain books of account and undergo the mandatory audits. ITR-4 is a simplified form that is available for small taxpayers (such as Individuals, HUFs, and Firms other than LLPs). The applicable taxpayers who file ITR-4 are not required to manage the financial records, including spreadsheets, profit and loss statements, and balance sheets. The small taxpayers who opt for the presumptive taxation scheme under Section 44AD, 44ADA, or 44AE file ITR-4 instead of ITR-3. The exact return filing form depends on the taxpayer's profession, business structure, turnover, and method of tax calculation.

Due Dates for ITR-3 and ITR-4

Missing the deadlines for ITR-3 and ITR-4 triggers heavy penalties, interest, and loss of certain benefits. Here is the complete table for due dates or ITR-3/ITR-4 filing in 2026 for FY 2025-26 (AY 2026-27):

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Latest ITR-3 and ITR-4 Updates for AY 2026-27

The registered taxpayers may experience differences related to structure and compliance while filing for ITR-3 or ITR-4 for AY 2026-27. These new updates are implemented on the Income Tax e-filing portal. The core updates at a glance:

CBDT Updates: The return framework has been modified by the Central Board of Direct Taxes (CBDT), which highlights that the due date for non-audit businesses and professionals has been shifted from 31st July to August 31 for non-audit to give extra time to small businesses to consolidate accounts.

Section 89A Relief Adjustment: The double taxation relief, which is provided under Section 89A, is completely shifted to ITR-2 and ITR-3 for foreign retirement accounts.

Reporting Requirements: Under Income From House Property, a new specific field has been introduced with the title "The amount of rent that cannot be realized." To claim HRA compliance, the taxpayers are required to provide the specific required documents, such as the PAN of the landlord and Form 124.

AIS & TIS Reconciliation: The pre-filled data mechanism has been modified to match the Annual Information Statement and taxpayer information summary. Before the final submission, the taxpayers can reconcile the difference between declared business/capital receipts and AIS data.

Taxpayer Compliance Updates: If taxpayers missed the belated return deadline (December 31, 2026), then the taxpayers can utilise ITR-U (Updated Return) by March 31, 2031. It is only applicable when you missed both the original and the belated return deadlines. However, late filing attracts penalties up to Rs 5,000 under Section 234F.

ITR-3: Meaning

ITR-3 is an income tax return form that applies to individuals and Hindu Undivided Families (HUFs). The applicable individuals and HUFs are required to file ITR-3 when they generate income from a proprietary business or profession. Because it covers the financial statement, it requires detailed disclosures of financial records, balance sheet, profit and loss account, and trading account.

Who Can File ITR-3?

The ITR-3 is filed by individuals and Hindu Undivided Families (HUFs) whose income source is from any profession or proprietary business. In this case, these categorized taxpayers can file for simple forms like ITR-1, ITR-2, and ITR-4. You must file ITR-3 if you meet the criteria below:

- If the income comes from professional practices or proprietary businesses.

- Applicable if not opting for presumptive taxation schemes.

- Partnership firms' partners who earn income from salary, bonus, commission, or interest (excluding LLPs).

- If income comes from more than one house property, capital gains, or dividends.

- The company's director holds unlisted equity shares at any time during the financial year.

- Income generation from Futures and Options (F&O) or intraday trading.

Who Cannot File ITR-3?

The companies and LLPs are not required to file the ITR-3 form. Instead, they are required to file a separate corporate or LLP return. The individuals and HUFs who are seeking "Presumptive Taxation Schemes, are also ineligible to file ITR-3, but they are required to file the ITR-4. Taxpayers whose sources of income are pension, salary, or house property are restricted from filing ITR-3 (should file ITR-1 or ITR-2).

ITR-4 (Sugam Form): Meaning

ITR-4 is a simplified income tax return form that is filed by resident individuals, HUFs, and partnership firms (excluding LLPs). Instead of filing ITR-3, these applicable taxpayers file ITR-4 when the total income is up to Rs 50 lakh and opt for the Presumptive Taxation Scheme (Sections 4AD, 44ADA, and 44AE). ITR-4 significantly reduces the headache of maintaining detailed bookkeeping.

Presumptive Taxation Scheme Explained

The Presumptive Taxation Scheme under Sections 44AD, 44ADA, and 44AE of the Income Tax Act is a simplified tax method. Under this scheme, small businesses, freelancers, and professionals enjoy simplified tax compliance, no bookkeeping, and no auditing. This scheme significantly avoids the headache of maintaining accounting records and undergoing audits. Once individuals or HUFs are categorised under this scheme, the government lets them pay tax on a presumed profit. It eliminates the requirement of calculating actual profit after detailed bookkeeping. Presumptive Taxation Scheme is broken down into three sections, as per the taxpayers' work:

- Small Businesses (Section 44AD)

- Professionals (Section 44ADA)

- Transporters (Section 44AAE)

Who Can File ITR-4?

You should file ITR-4 if you do not want to maintain financial records, and the following are the income sources:

- Presumptive business income categorized under Section 44AD or Section 44AE.

- Specified professionals (like doctors, freelancers, accountants, or engineers) under Section 44ADA with gross receipts up to Rs 50 lakh.

- Applicable if agricultural income is up to Rs 5,000, including rental income from up to two house properties.

- Income from long-term capital gains up to Rs 1.25 lakh.

Who Cannot File ITR-4?

The taxpayers are strictly ineligible to file the ITR-4 form if they meet the following categories:

- The Non-Resident Indians (NRIs) who do not hold residency status.

- If the income threshold limit exceeds Rs 50 lakh.

- You have short-term capital gains or long-term capital gains that exceed Rs 1.25 lakh.

- If you are a director of a company and hold unlisted equity shares in the preceding financial year.

- You hold the foreign income/assets.

- Income comes from more than two house properties.

- Earn income from gambling, horse racing, virtual digital assets, or lotteries.

- Your tax has been deducted under Section 194N (cash withdrawal TDS).

ITR-3 vs ITR-4: Detailed Comparison

Here is a quick comparison summary of ITR-3 vs. ITR-4.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Which Form You Should Choose: ITR-3 vs ITR-4

Whether you need to file ITR-3 or ITR-4, it completely depends on your income type, turnover size, and your accounting records. Both forms are filed by individuals and Hindu Undivided Families (HUFs). But the difference comes when business or professional income is under presumptive taxation, or businesses/professionals are required to maintain accounting records, audits, foreign assets, and other reporting.

When to Choose ITR-3?

An individual or HUF is required to file the ITR-3 form when its income profile is complex. Even filing this form becomes mandatory when you need to report actual business or professional profits. If you are a company's director, trade in F&O, or hold unlisted equity shares, you must file this form to declare the actual income.

For example, you work as a Mumbai-based freelance marketing consultant. Your income comes from client projects, and you also trade F&Os on the stock market. Although you want to declare the actual business expenses and trading losses. At this stage, you need to file the ITR-3 because this income does not come under the presumptive taxation scheme and requires detailed reporting.

When to Choose ITR-4?

Selecting the ITR-4 is ideal for those who do not want to manage the compliance complexities, including those who do not want to maintain books of account, audits, etc. This form is filed by small businesses and professionals who want to report the minimum percentage of their turnover under the presumptive taxation scheme. ITR-4 avoids the headache of maintaining accounting records and tax audits.

For example, you are working as a small freelance tutor in Delhi and want to declare profit on a presumptive basis, required to file the ITR-4. In this case, you are not strictly required to fulfill the requirements for financial records.

Consequences of Missing the ITR Filing Deadline

On time ITR form filing is important to avoid the possible late-filing penalty. After missing the primary deadline, the taxpayers can file a belated return, but it attracts late-filing monetary charges, including interest on unpaid taxes. The major consequences depend on how late you file and your financial situation:

1. Late filing under Section 234F

Often, taxpayers file a belated return after missing the original due date. However, a belated return triggers a late-filing penalty, which depends on the income of taxpayers. If your income is over Rs 5 lakh, you may need to pay a Rs 5,000 late fee. If income falls between Rs 2.5 lakh and Rs 5 lakh, then you are only required to pay Rs 1,000. In case the income is below the tax table limit, there is no need to pay a late filing penalty.

2. Interest on Unpaid Taxes

Interest will be applied at 1% per month or part of a month on the unpaid tax amount if you have any outstanding tax dues and missed the original due date for ITR filing.

3. Loss of Carry-Forward Benefits

Avoiding the deadline also means missing the opportunity to carry forward losses to offset future gains if your investments or business venture suffered losses.

4. Option After the Final Deadline

If a taxpayer missed the original deadline as well as the belated deadline, they can still file an Updated Return, also called ITR-U. However, it attracts a 25% to 50% late filing penalty. If the default is related to ITR filing, the taxpayers may face strict legal action, even imprisonment in extreme cases.

Conclusion

An ITR (Income Tax Return) is an official form submitted to the Income Tax Department that details annual income, deductions, investments, and taxes paid. The form is used to submit the financial statement to the tax authority annually. Meanwhile, ITR-3 is designed for individuals and HUFs whose source of income is business or professional activities. But ITR-3 filing taxpayers are required to maintain detailed records and comply with strict formalities, such as maintaining books of account and undergoing audits.

While ITR-4 is a simplified financial statement form for small taxpayers under presumptive taxation. However, missing the original due date for ITR filing triggers hefty penalties, interest, and loss of carry-forward benefits. To make ITR filing smooth and accurate for Y 2025-26 (AY 2026-27), JustStart offers expert guidance to taxpayers. From selection support to compliance assistance and hassle-free ITR filing on a single platform.

Frequently Asked Questions (FAQs)

Q1. What is the difference between ITR-3 and ITR-4?

Ans. ITR-3 and ITR-4 are both applicable to individuals, HUFs, and Firms (excluding LLPs) whose income source is business or professional activities. ITR-3 is for those who maintain detailed books of account and want to declare actual income. Whereas ITR-4 is for small businesses or professionals who are opting for presumptive taxation.

Q2. Can freelancers file ITR-4?

Ans. Yes, freelancers can absolutely file the Sugam (ITR-4) if they opt for the presumptive taxation scheme under Section 44ADA of the Income Tax Act. It significantly saves them from the complex books of account.

Q3. Can I get a refund for late ITR filing?

Ans. Yes, you can claim the tax refund, but it depends on how late you file the ITR. If you file a belated return, you can claim a tax refund. If you missed the December 31st deadline and go for filing an updated return, then you cannot claim a tax refund.

Q4. Is a tax audit compulsory for ITR-4?

Ans. No, a tax audit is not mandatory for the ITR-4 taxpayers, as it is designed for those who opt for the presumptive taxation scheme. ITR-4 taxpayers are free from keeping order of books of account and undergoing audit requirements.

Q5. Can doctors file ITR-4?

Ans. Yes, the doctors in India are eligible to file the ITR-4 form if they opt for the presumptive taxation scheme under Section 44ADA.

Q6. Which ITR form is filed by LLPs?

Ans. Limited Liability Partnerships (LLPs) are required to submit their financial statements using the ITR-5 form.

Q7. What is the due date for ITR-4 in 2026?

Ans. The original due date for ITR-4 depends on the tax audit requirement. If an audit is required, the form must be filed by August 31, 2026; in case of a non-audit, it must be filed by October 31, 2026.

Q8. Is GST registration mandatory for ITR filing?

Ans. GST registration is not compulsory for ITR filing, as both have different perspectives. GST is for indirect tax on goods or services, whereas ITR is for direct tax. ITR can be filed without a GST number.

Q9. What are the benefits of the presumptive taxation scheme?

Ans. The presumptive taxation scheme is designed for small businesses or professionals, and it is governed under Sections 44ADA and 44AD. Under these schemes, the eligible taxpayers declare a fixed percentage of their turnover as profit.

Q10. Where to declare the foreign income in ITR?

Ans. The foreign income is generally declared in Schedule FSI by using the ITR-2 or ITR-3 form. If a taxpayer also has a foreign asset, they must declare it in Schedule FA.